What is Life Insurance?

Life Insurance is a contract between an insurer and a policy owner. A life insurance policy guarantees that the insurer pays a sum of money to named beneficiaries when the insured dies in exchange for the premium paid by the policyholder during his lifetime.

For the contract to be enforceable, a life insurance application must accurately disclose the insured’s past and present health conditions and high-risk activities.

What is Life Insurance

Life Insurance is a legally binding contract that pays a death benefit

Life Insurance is a legally binding contract between an insurer and a policy owner. A life insurance policy guarantees that the insurer pays a sum of money to named beneficiaries when the insured dies in exchange for the premium paid by the policyholder during his lifetime.

Policies have several inherent features:

The age of the insured person should be at least 21 years.

A life insurance policy should be purchased in the name of the policy owner, unless a minor is named as the beneficiary. If the insured is already married, only one spouse can be named as the beneficiary. The relatives of the insured person can be nominated as beneficiaries for a maximum of five children.

Premium payments must be made on an annual basis otherwise they will lapse.

What is Life Insurance policy?

A life insurance policy is usually in the form of a fixed death benefit or a variable death benefit. A fixed death benefit is a guaranteed amount paid by the insurer to the policy owner, such as $500,000, when the insured dies. A variable death benefit is an amount that varies according to the insured’s health and life expectancy.

The policy owner can change or add a named beneficiary before or after the termination of the contract.

Also Read: How To Apply For A Best Personal Loan in 2022

How much life insurance do you need?

You need to make some basic life insurance decisions to figure out how muchinsurance you need to buy. The following are general guidelines that will help you determine the right amount of Insurance for your family.

Life Insurance contract

To ensure that you receive your full life insurance payout, the insurance company must agree to settle the policy in one of three ways: payment through death, gift of life or death benefit.

Because life insurance policies are generally non-cancelable, if one of the contract options is not exercised, the policy owner pays the insurer for the remaining years of the policy, up to the end of the insured’s life. is bound to pay.

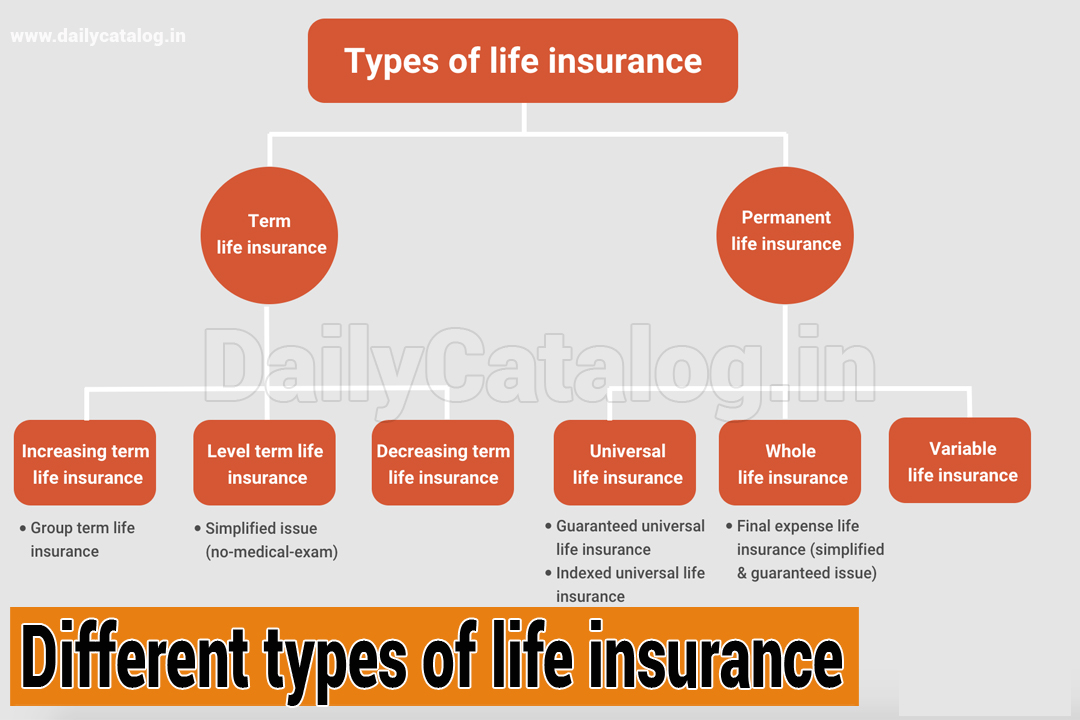

What are the different types of life insurance?

A life insurance contract can be written in annuity contract, insurance policy or policy loan. The life insurance contract is generally selected based on the information provided by the insured to the insurance company.

different types of life insurance

- Insurance companies and their products

- Homeowner’s Insurance

- Children’s Life Insurance

- Single Woman Life Insurance

- Insurance coverage for major household assets such as automobiles, boats and ATVs

Life insurance is generally required for everyone. If you own a small business, insurance is usually mandatory for all employees. However, there are some reasons why this may not be necessary or recommended.

In some cases, some large corporations offer “deferred” insurance, which pays out a lump sum upon the insured’s death. If the insured does not die within a certain period, the money is lost forever.

There are also term insurance policies. Term insurance is a less expensive form of insurance. For example, you can buy a 30-year term life policy for $1,000,000 at a monthly premium of $15.

Who needs life insurance?

How much life insurance do you need?

Six to 10 times annual salary: insurance companies require a insurance policy to be more than six to 10 times the employee’s annual salary for the policy owner. If the company’s market value is more than six times the annual salary, it is less likely that the company will offer a reduced policy.

Compare 10% of salary to Insurance premium: This is a general guideline. Insurance companies determine how much coverage an employee needs based on factors such as the insured’s age and health, and whether they smoke or drink.

When do you need life insurance?

Age over 35 years: If you are planning to retire in the next five years, then insurance companies should take you adequate insurance for your dependents.

If you die.

- How to get rights

- policy for you

- What you should know about life insurance

- part of

- Guide to Life Insurance

- Insurance take-away

- How many years do you need life insurance?

- Get your free quote

What is Life Insurance? Most insurance companies say that a reasonable amount for insurance is six to 10 times the amount of annual salary. Another way to calculate the amount ofinsurance required is to multiply your annual salary by the number of years until retirement. Signature Insurance Guide to Insurance Insurance Policies and Companies Athos Logo Insurance Take-Away How many years do you need insurance? Get your free quote

Conclusion

There is no medical website. Our facts are based on research, not opinion. In this chapter we will look at suicide by working with the five most popular methods of suicide. Why not work with someone who is working?

Conclusion

Each of the five means of suicide can be prevented, be it a gun, poison, cutting, drowning or jumping from a building. Why? Because each method has a lethal dose. In addition to being in a coma, or in the case of poisoning, in the case of passing out, each method can result in death.

Let’s take a look at some suicide prevention tips, as each method has something that needs to be addressed. We’ll also discuss how to work with all five methods to prevent them.

Factors Affecting Life Insurance Premiums

Now that you know what life insurance is and why you need it, explore the factors that can affect life insurance premiums:

- Age: One of the major factors that affect the premium of a insurance plan is your age. Life insurance premiums are lower for younger people and gradually increase with age

- Gender: Studies show that women live longer than men. Therefore, insurance premiums are lower for women than for men

- Health condition: Your current and past health conditions can determine the premium for your insurance plan. If you have a pre-existing illness or have suffered from an illness in the past that may re-emerge or affect your current health, you will be charged a higher premium.

- Family Health History: Chances of suffering from a disease that runs in your family are high. So, if a hereditary disease runs in your family, you may have to pay a higher premium

- Smoking and drinking alcohol: Lifestyle habits like smoking and drinking alcohol can affect your health and lead to multiple health problems. Hence, insurance companies charge higher premiums for individuals who smoke or drink alcohol

- Type of coverage: The type of coverage you choose can increase or decrease the premium of a insurance plan. If you add any riders to your plan, the premium will increase. A longer policy term may also result in a higher premium compared to a shorter term. In addition, the insurance plan you choose also affects the premium. For instance, term insurance is the cheapest form of insurance

- Amount of coverage: Higher sum assured will result in higher premium and vice versa

- Occupation: If you work in a high-risk job, your insurance plan premium will be higher than others. For example, if you work in construction or if your job exposes you to any kind of risk, such as regular exposure to chemicals, the insurance company will charge a higher premium.

Let’s understand some of the commonly used terms in life insurance:

Life Assured: It is the person who is covered under the insurance policy

terms in life insurance

Proposer: He is the person who pays the premiums of the policy. For example: If you bought a policy for yourself, you are both the life insured and the proposer. Similarly, if you buy an insurance policy for a family member, you are the proposer and the family member is the life insured.

- Nominee or Beneficiary: The person you designate while purchasing the policy to receive the benefits of your insurance policy, in your absence.

- Insurance Company: An insurance company that sells life insurance policies is called an underwriter (for example, ICICI Prudential Life Insurance).

- Life Cover: It is the amount that the insurer will pay to your nominee in case of an unfortunate event.

- Maturity Benefit: For a Protection + Savings policy, the insurer pays a certain amount on maturity of the policy. This amount is known as maturity amount.

- Premium: Premium is the amount you pay to the insurance company to get the benefits of the insurance policy. These payments can be made on a regular basis during the policy term, for a limited number of years or just once, depending on the options available under the policy you choose.

- Premium Payment Term: The number of years for which you pay the premium is known as the premium payment term.

- Policy Term: The number of years for which the life cover continues.

How to choose the right life insurance company in India?

It is important to choose an insurance plan that meets one’s insurance needs as well as fits within the budget. However, one should not be swayed by low premiums while buying an insurance plan, he/she should thoroughly research the insurance company and identify its insurance needs before buying a life insurance plan.

There are many life insurance companies to choose from. Here are some factors that you should consider before choosing a particular insurance company:

1. Claim Settlement Ratio: Claim Settlement Ratio or CSR of an insurance company shows its effectiveness and reliability. The claim settlement ratio of an insurance company shows the number of claims settled in a financial year against the total number of claims. This ratio helps to find out the proactivity of the insurance company in terms of settlement of claims. A high claim settlement ratio of an insurance company shows the dedication of the insurance company in terms of settlement of claims. This shows the loyalty of the insurance company towards its customers. Insurance Regulatory and Development Authority (IRDA) reviews the claim settlement ratio of insurance companies.

2. Customer Care Service: Customer care service is an important factor to consider while purchasing an insurance plan. One should always choose an insurance company that provides good quality customer care service. While purchasing a life insurance policy, a customer should always keep in mind that 24×7 customer care service is available to resolve all their queries and provide assistance when needed.

3. Availability of Riders: Life insurance riders are additional benefits that insurance companies offer while purchasing life insurance plans. They are purchased with plans that increase the premium and they also increase the life cover. One should always ensure that the insurance company offers riders or an option to add riders to the insurance policy. Some of the common riders offered by insurance companies are Critical Illness Rider, Accidental Death Benefit Rider, Accidental Total or Permanent Disability Rider and Waiver of Premium Rider. With these optional additional riders offered one can make better decisions by choosing the best plan and riders offered with it.

4. Company Persistence Ratio: Company Persistence Ratio shows the number of policyholders who renew their life insurance policies with the same insurance company. It is the ratio of the total number of policyholders to the number of policyholders who have renewed their policies. A company’s persistence ratio indicates customer satisfaction with an insurance provider. The insurance company’s persistence ratio is monitored by the Insurance Regulatory and Development Authority (IRDA).

5. Feedback and Reviews: Usually the applicant insurance company does not pay attention to the feedback and reviews received from the customers. One should always go through the feedback/reviews of the company and pay attention to the complaints/bad reviews. This allows the applicant to understand which insurance company is better than others and if the insurance company should be chosen or not

How to find the best life insurance policy for you

With a wide variety of life insurance policies available, deciding on the right policy can be a challenge for any buyer. Don’t go it alone when trying to find the best life insurance policy. Financial advisors and experienced life insurance agents have the background to help you make the right decision based on your financial goals and budget.

See Financial Strength Rating.

A strong financial strength rating is more than just peace of mind that a company won’t go out of business decades from now. Insurers with greater financial strength are less likely to need to increase internal policy costs and premiums in response to challenging financial times.

Ratings are available from agencies such as Standard & Poor’s and AM Best and are usually found on insurance companies’ websites.

Choose life insurance as part of a larger financial plan.

A financial advisor can explain the best life insurance options in terms of your larger personal financial goals.

Don’t assume that insurance companies offer competitive pricing for everyone.

Life insurance companies want your business, but they all operate from their own playbooks. Premiums can vary greatly and, for cash value policies, cash value growth can vary widely across companies and policies.

Be aware that a life insurance quote for a cash value policy may not reflect what you will actually pay over the years to keep the policy in force.

“Current rules in some states and for some products allow insurance companies to ‘quote’ lower premiums while charging higher prices — without disclosing that you may need to pay additional premiums later to avoid a loss,” warns Barry Flagg, founder of Veralytic. is . .

Insist that cost disclosures for universal life insurance be included in any proposals.

A life insurance quote reflects what you will be billed for, but it doesn’t tell you anything about the internal costs of the policy, such as expenses and fees, and the actual cost of insurance charged in the policy.

Be sure to insist that any universal life insurance illustration include detailed expense pages or policy accounting pages. A product with a low premium quote may have a higher intrinsic value, which can slow down your cash value growth.

Find out if you want life insurance riders

Life insurance companies usually allow you to add additional coverage to your policy through life insurance riders. These riders can include benefits you can use while you’re alive, such as accelerated death benefits, long-term care, term life conversion, and premium waivers if you become disabled.

Adding a rider can increase the cost of life insurance. If you are interested in increasing coverage through a life insurance rider, ask your life insurance agent to explain the options.

Let’s understand how life insurance works:

In today’s era, having a life insurance policy is a must for everyone as it is the best way to secure their future along with their loved ones. There are various types of insurance policies available in the market. However, before choosing one, it is important to understand how a life insurance policy works. Let’s look at an example to understand how insurance works:

Now, let’s look at an example:

Mr. Kumar (life assured) pays an annual sum (premium) over 5 years (premium payment term) to ICICI Prudential Insurance (insurer) to ensure that his wife (nominee) gets a certain sum assured (life cover). Lumpsum amount on maturity in case of any unfortunate event during 10 years or survival at the end of policy term.

insurance not only covers the risk arising out of an unfortunate event, but also gives you additional benefits like tax benefits, savings and wealth creation over time. A suitable insurance plan from a reliable company can help one get long-term risk cover plus savings, i.e. dual benefits from one solution.